All you need to know about LSD/LP regulation

All you need to know about LSD/LP regulation

Executive Summary

1) LP Tokens and Staking derivatives are digital primitives that were only recently introduced as financial instruments in decentralized finance (DeFi). Each asset has mixed properties both as security and commodity.

LP tokens can be viewed as a mutual fund (classifying it as a security) but the underlying tokens in the pool are not further invested in other enterprises, meaning the tokens are only locked in a “pool” to follow a constant function market maker (classifying it as a commodity).

Staking derivatives can be viewed as a treasury bond that accrues interest (classifying it as a security), but it is distributed across multiple “pools” that contributes to the security-enhancing mechanism for the chain (classifying it as a commodity).

2) Given the recent turmoil in the industry, harsher scrutiny from regulators is expected in the next five years and will lead to more specific categorizations of assets. LP tokens are expected to be categorized more as a security, whereas staking derivatives as commodities.

Higher regulatory interest is perceived as a direct threat by many industry opinion leaders (drawing their case from OFAC and Tornado Cash) that will compromise the very core ethos of crypto.

However, increased interest in the industry can spur deeper investigation of various assets, as opposed to regulating them in a one-size-fits-all manner. In this sense, it will start out as various asset tokens (LP, staking, governance, utility, options, etc.) being individually investigated by the court but the regulators will eventually call for a new crypto-versioned Howey test in the long term.

3) Infrastructure-level and Protocol level regulation won’t take place on public blockchains, but US regulatory regimes will still exert their influence through centralized entities such as Tether or Circle, as well as CBDCs that interact with the public blockchains not affecting the LP/Staking landscape.

Regulating blockchain and the infrastructure itself is nearly impossible considering the distributed/anonymous nature of blockchains. “Interacting” with certain validators or protocol smart contracts can still kick in (as it did with Tornado Cash), but is expected to be very limited because the regulatory regime is focused primarily on anti-money laundering infrastructure rather than identifying each customer/address per protocol.

Regulating frontends of DeFi protocols (that are hosted and owned in the US) is a possibility, but requires too much regulatory resources and so is not an efficient mode of regulation; thus we don’t see it as a viable future in the next 5 years.

Intro

We originally started on this project as a “SEC vs CFTC” debate, but quickly decided this wasn’t much fun nor informative as the debate would be more of an ethos debate. So we wanted to make sure our research encapsulates two structural aspects of the crypto regulation issue: 1) The advent of various digital financial primitives that are fairly nascent not only in the ecosystem but also within the history of finance and thus haven't been investigated deeply enough and 2) regulatory milestones that could shape how DeFi will be interacting with the greater masses such as OFAC’s sanctions on Tornado Cash or government oversight of Circle and Tether. Now the question switched to: Given this set of irresistible forces driving this industry, what future do we imagine for these new digital primitives in the future? More specifically, will LP tokens and staking derivatives be regulated as securities over the next five years? In what form will the regulation take place?

This piece centers around these three main questions:

Will LP tokens and liquid staking tokens be considered as securities by regulators—assuming most tokens including ETH and BTC will be considered as commodities and regulated under the jurisdiction of the CFTC?

Will KYC/AML measures be implemented (on staking derivatives and DEXes) on the developers/service providers/validators’ ends such as what happened with Tornado Cash?

Will KYC/AML measures be applied more strictly on users and consumers, via regulating frontend interfaces of the DeFi platforms upon US customers?

(We will be assuming that in the near future most of retail will already have gone through some KYC measures using centralized exchanges.)

Preliminaries

What defines security?

The Howey Test (that resulted from the case “SEC v. W. J. Howey Co.”) requires that a financial contract is a security if all of the following conditions hold; it must be:

1) An investment of money

2) In a common enterprise

3) With the expectation of profit

4) To be derived from the efforts of others.

Under this Howey Test, securities can be classified into the following four categories:

Equity securities: These securities represent a share of ownership in a company, trust, or partnership (think capital stock). As a result, holders of equity securities can benefit from earnings in the form of dividends, which fluctuate based on the market, and capital gains when they sell the securities.

Debt securities: With debt securities, companies can borrow funds from investors and repay the loan with interest. Examples of debt securities are bonds and promissory notes.

Hybrid securities: These securities are just as the name suggests – a combination of debt and equity securities. An example of a hybrid security is a convertible bond, which can be converted into shares of stock for the company issuing the bond.

Derivative securities: These are contracts between two or more parties. Their value depends on the price of an underlying asset.

(Embroker)

How does a security being categorized as a security change the regulatory landscape around it?

Commodities (such as gold, corn, or copper) are generally regulated less strictly than securities. If these tokens were considered securities, this would imply oversight by the SEC instead of the CFTC and much more through disclosure and reporting requirements - on par with the extensive regulation seen in traditional finance (TradFi).

The Debate #1: Will LP tokens and liquid staking tokens be considered as commodities by regulators (assuming most tokens, like ETH and BTC, will be considered commodities and regulated by the CFTC)?

No (LP/liquid staking tokens will be a security): Let’s first take a look at LP tokens - what are they? They’re an asset received as proof of providing liquidity to an AMM (Uniswap, Curve, etc). You could consider them to be a derivative valued from the underlying asset deposited. They are closely linked by nature to markets people enter with the purpose of trading/investing and received as a byproduct of providing liquidity, which in itself is often done for investment purposes. These characteristics should already be enough to raise the eyebrows of regulators, but it is the common uses of LP tokens that cement their probable future status as securities. On Uniswap v3, given that liquidity can be deposited in specific price ranges users often strategically place their liquidity for a variety of strategies. This can range from most commonly aiming to maximize trading fees received, but also for other purposes such as to simulate a limit order. This would be done by depositing all of the liquidity in a single asset within a given range. If the relative price of the assets in the pool crosses this range, the participant would then see their position fully converted into the pool’s other asset, at the relative price they deposited their liquidity at. All of these hypothetical positions and strategies are contained within the LP token received by the user, giving them intrinsic value.

Additionally, these tokens are very often further leveraged and staked on DeFi platforms for yield farming, which in itself suggests the expectation of investment returns. For example, using LP tokens as collateral on Aave or staking them on Convex. The possibilities are endless once the LP tokens leave their initial venue.

These are just some of the key characteristics of LP tokens, which make them, among the universe of crypto assets, a low-hanging fruit for regulators to consider as a security. Lastly, it’s interesting to reference this article from the now basically defunct CREAM Finance, which discusses the investment purposes behind providing liquidity and draws parallels to traditional finance markets.

“The way we see it, there is no reason for LP positions to sit idle in yield farmers’ wallets. This is capital inefficiency at its worst. LP positions are valuable collateral. As collateral they will be used to generate further liquidity and earnings for both the original farmer and other market participants. Providing liquidity in DeFi is a valuable service — it’s akin to running a small (and sometimes not so small) business. Providing liquidity generates real cash flows and in traditional financial markets, cash flow generating businesses can be leveraged. Business owners borrow against their current assets and future cash flows to grow. C.R.E.A.M. wants to empower this growth for the entire DeFi market.”

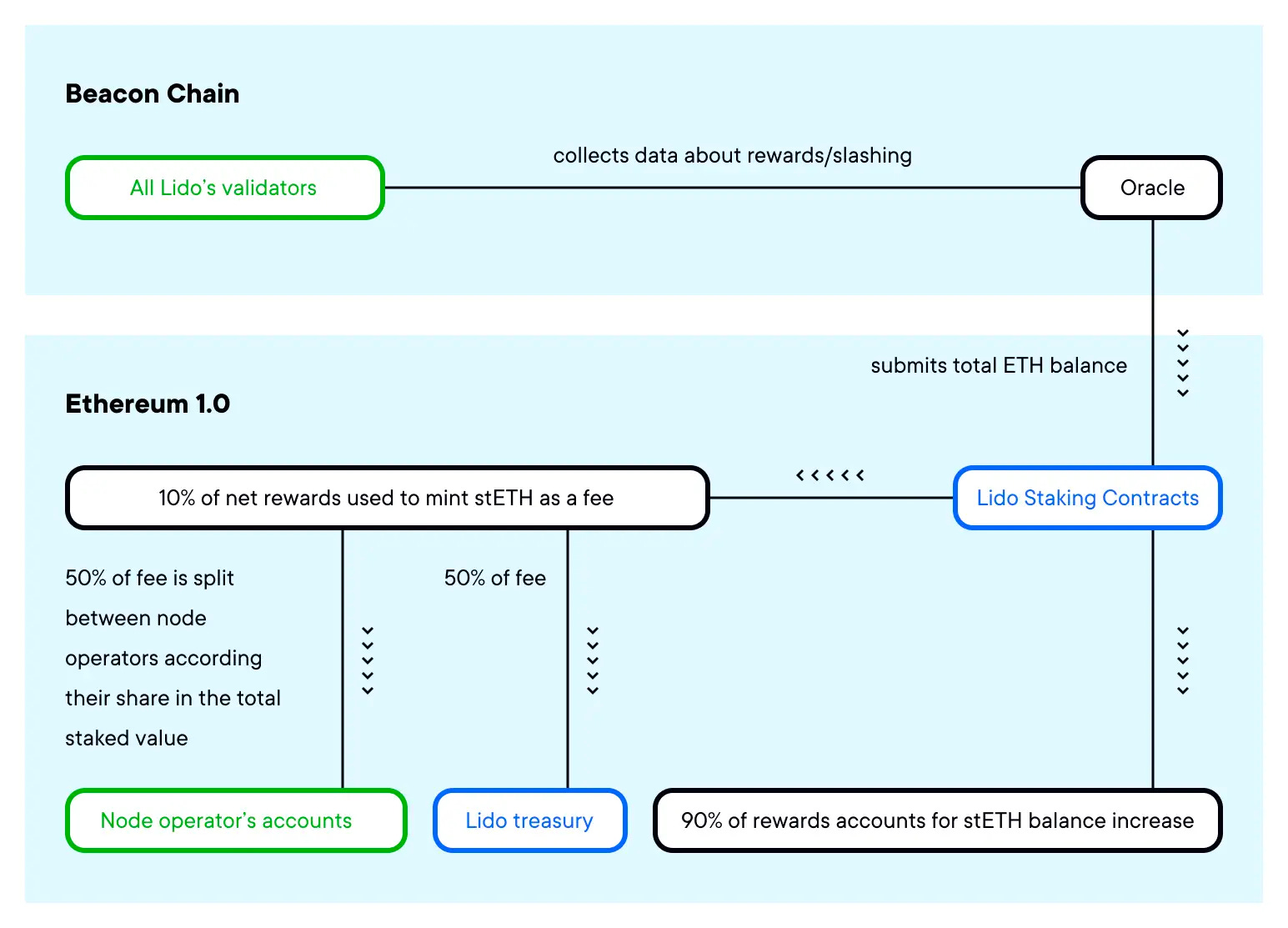

Next, we examine liquid staking tokens. These were created in part to address the issue of lockup periods when staking crypto, and, analogous to LP tokens, to allow participants to access liquidity and earn yields on their existing assets. Particularly, most forms of liquid staking tokens (e.g. tokens offered by Lido) allow the holder to accrue staking rewards on their held liquid staking tokens. On top of this, holders can accumulate further rewards, similarly as with yield farming with LP tokens, by depositing their liquid staking tokens on other DeFi platforms. If we look at the websites for some of these platforms such as Lido, we clearly see an advertised expectation of profit (with a listed APR) derived from what is very arguably a common enterprise and the efforts of others (other users adding liquidity to the pool).

These are already strong arguments that regulators could use to regulate these types of tokens as securities. Another notable element to the story here is the history of the usage of these tokens as speculative instruments on the future price of an underlying crypto asset. For example, when stETH traded at a discount during certain periods pre-merge, this was seen by some as a sign that the market was pricing in a lower value for post-merge ETH valuation. In that sense, we could consider stETH to be a forward contract on ETH with the unspecified delivery date of when ETH unstaking will be enabled.

One last example of an investment strategy involving these tokens: their use for the creation of a leveraged position in the underlying asset: example – deposit ETH with Lido, receive stETH, deposit stETH as collateral on Aave to borrow ETH, which you deposit on Lido to receive stETH, so on and so forth. (This implies significant risk in the case of stETH price deviating much from ETH price.)

Yes (LSD/LP will be commodities):

Surprisingly enough, none of the four prongs of the Howey Test seems to be applicable in the case of LP tokens and staking derivative tokens. We will see why as we constantly compare these assets to those 9 tokens (AMP, RLY, DDX, XYO, RGT, LCX, POWR, DFX, and KROM) that were explicitly mentioned in the recent SEC’s complaint that charges three former Coinbase employees of insider trading over 25 digital assets.

An investment of money. What seems to be most evidently fulfilling is in fact not the case here. Firstly, this is because LP tokens or staking derivatives are in themselves not an investment of “money” as compared to those 9 tokens that were literally put on sale in exchange of US dollars through ICO. LP tokens call for some basket of crypto assets, but they are not “money” to begin with. Staking tokens also require native tokens such as ETH or SOL, but not stablecoins. Now there are exceptions to this where the pair includes one or more stablecoin, but otherwise, this argument is pretty solid to start with. Moreover, it is also worth noting that while “fungibility” is one of the critical components of a security, many LP tokens such as Uniswap V3 have started using Non-fungible tokens as LP tokens, which limits a further utilization of the asset as opposed to fungible LP tokens. But even for fungible LP tokens, fungibility and the following extensive utility cannot be a sufficient condition for them being categorized as securities, because ultimately all commodities also can be used as collateral, lending and other financial activities.

In a common enterprise. According to Revak v. SEC Realty Corp., Federal courts require that there be either horizontal commonality or vertical commonality in a project to satisfy being a common enterprise. Horizontal commonality exists where each individual investor’s fortunes are tied to the fortunes of other investors by the pooling of assets, often combined with the pro-rata distribution of profits. Vertical commonality focuses on the relationship between an asset’s promoter (either effort itself or the promoter’s fortune) and the asset’s investors.

First, vertical commonality is not applicable to either the LP token nor the staking derivative. This is because there is no such promoter in the dynamics. Individuals are interacting with the smart contract that was deployed on the blockchain.

LP tokens would easily satisfy horizontal commonality since each LP token is treated uniformly and the underlying assets are pooled together. However, vertical commonality is not satisfied because LP tokens don’t have a promoter whose fortune is aligned with the token holders. A counterargument to this would be the existence of an operating team behind DEXes, but even in that case governance token would represent any share in such a common enterprise, not the LP tokens. LP token only represents a share of the liquidity pool, not the enterprise itself.

Staking pools are slightly different in that even horizontal commonality does not apply. This is because staking pools are not aggregated into a uniform pool, but into separate pools of certain size–32 ETH in the case of Lido. This implies that although a staking derivative may be representing one corresponding underlying asset, the inner workings does not guarantee a single pool that amasses those assets into one pool but rather separate staking pools that are directly interacting with the staking derivative protocol contract. Moreover, vertical commonality is also in question, for staking derivative tokens does not have an evident promoter but only sets of smart contracts that are preprogrammed to behave in a certain way.

Furthermore, the fact that the assets that are deposited are funneled to node operators that utilizes those assets to support the overall security of the whole chain makes it harder to determine where the common enterprise lies. As an example, Lido protocol has a diverse set of node operators: Node Operator Numbers for Lido is 29 for Ethereum, 26 for Polkadot, 6 for Polygon (Source) (Stats)

With the expectation of profit. There are many reasons why certain investors are converting their assets into either LP tokens or staking derivatives. Let’s look at LP tokens. Many protocols are providing liquidity literally for the sake of providing enough liquidity to their tokens such as when they newly launch a token, in which case they are doing so even with an expectation of loss. This is coming from the fact that even without the trading fees accrued, liquidity pools already have a primary goal of providing a market for exchange and discovering price of certain assets. Furthermore, some investors also prefer investing in liquidity pools because it is one of the most efficient ways of holding a portfolio of assets of their choice to their predetermined proportion.This includes normal LP pools including Uniswap V2, V3 and geometric market making pools such as Balancer pools or Curve Crypto Pools. In this case, these LP token holders are not necessarily expecting profit, but are utilizing the automatic portfolio management feature of these pools.

Similar logic can be applied to staking derivative tokens. Staking derivative tokens are, by their name, more a derivative instrument than being a security itself. For example, someone with reasons to stake ETH (say they just love Ethereum so much and want to guard its security), while they could literally run a node themselves and stake 32 ETH, would also want to liquidate their “staked” position. Liquid Staking Derivatives provide a perfect way for them to liquidate such positions and be more capital-efficient. Thus such participants are not expecting profit from such action of minting new stETH tokens but rather using it just as a means to hedge their exposure to the asset. In that sense, the more important question here would be: Is Ethereum a security? If it is classified as such, then stETH will be classified as equity derivative and thus regulated by SEC. If not, it will just be a typical derivative over a commodity.

To be derived from the efforts of others. Similar to the second prong, but both LP tokens and staking derivative tokens don’t require an additional effort of others to operate. The smart contract that locks a set of certain assets works on its own as programmed, while some of the gas fees are paid by the users. There may be DAOs who are implementing those contracts and operating the protocol, but it is important to note that all the work is mostly finalized preceding any creation of LP tokens or staking derivative tokens, i.e. the assets that are locked in the contract in exchange for the LP tokens or the staking derivative tokens are not used in anyway to promote or incentivize such work of implementation. This is critical as can be seen in the recent SEC complaint, where the fact that the ICO investment was used to promote further progress of the protocol was an important component of making those 9 tokens securities.

In the end, these staking pools and liquidity providing pools are all just some number that are cryptographically connected to certain addresses that represent the contract. These smart contracts allow us to make “artificial code machines'' that manage a certain pool of assets even without a “common enterprise.” In that sense, how we define and accept decentralization as an industry is very critical. Not all DeFi protocols will be created equal.

Just as a side note, the SEC is already facing vagueness when they try to apply the Howey Test even to normal tokens (governance token sorts). A more plausible future is a joint committee between SEC and CFTC (like how Former CFTC Chair puts it) or an entirely new committee. Liquidity Providing pools and staking derivatives are an entirely new digital financial primitive.

Will KYC/AML be implemented (on staking derivatives and DEXes) on the developer and service providers, validators such as what happened with Tornado Cash?

Yes: Although the most recent bills, especially the leaked draft of the DCCPA that circulated in October, appear to have softened language relating to people who code / design DeFi platforms, they are still aiming to bring TradFi-like regulation to DeFi. Particularly, they impose human involvement in every decentralized platform, whether that is a DAO or DEX, by mandating compliance officers, registration with the CFTC through a central entity, and reserving the right for the CFTC to charge fees to these entities in order to “fund its oversight”. In official documents, these intentions also come through in the language on the Senate Committee’s website’s description of this upcoming bill. Overall, this generated significant pushback from crypto communities - see this Twitter thread from October, written by a pro-DeFi activist DAO. Notably, the regulation in the pipeline will in effect prevent the creation of anonymous DeFi projects, meaning all projects legal in the US will necessarily be KYCd.

Given the recent events surrounding the collapse of FTX, it’s also very reasonable to assume that legislators will take an even harder line on crypto institutions, brokers, exchanges, and DeFi platforms, citing FTX’s stunning implosion as the justification that investors need more protection and guardrails. This is particularly ironic given that prior to this collapse, SBF was seen as more “on the side of the regulators” and was increasingly unpopular in pro-DeFi circles due to his views on the role regulators should have in crypto. However, his lack of transparency and the still unclear timeline of the movement of funds between FTX and Alameda Research will only provide regulators for more ammunition and justification on why they should crack down on crypto platforms and regulate them similarly to TradFi financial institutions.

Additionally, CFTC complaints on the Ooki DAO case shows DeFi does not guarantee immunization. Recent CFTC commissioner Dan Berkovitz quotes: "[n]ot only do I think that unlicensed DeFi markets for derivative instruments are a bad idea, I also do not see how they are legal under the CEA." A few years prior to that, a CFTC spokesperson stated in response to questions about Augur—a DeFi prediction market offering, among other things, assassination contracts—that "[w]hile I won't comment on the business model of any specific company, I can say generally that offering or facilitating a product or activity by way of releasing code onto a blockchain does not absolve any entity or individual from complying with pertinent laws or CFTC regulations[.]" The CFTC's unincorporated association theory of liability is not unique: The SEC's 2017 DAO Report pointed out that Section 3(a)(1) of the Securities Exchange Act of 1934 defines an "exchange" as "any … association, or group of persons, whether incorporated or unincorporated…."

No: The more plausible future is where most of the world’s governments will engage only with CeFi players/CEXes.

We can assume most governments around the world have now realized that regulating the interface between crypto assets and fiat currencies is the key here. This includes imposing KYC/AML measures on centralized exchanges, monitoring the issuance/collateral management of Circle/Tether and their contracts. Once they can track how money entered into the system and where it flowed, and without interaction with the mixers, regulators can pretty much track that money. This is why DCEA and DCCPA all focus on digital commodities exchanges and how to make sure KYC/AML measures are implemented thoroughly. Regulators also having strong legislations around stablecoin issuers such as Tether and Circle is not surprising because they literally convert certain dollar-based assets into an asset on-chain.

Regulators are more focused on reducing system risks stemming from the class of assets which can still be achieved by regulating the gateways, namely the exchanges and service providers. For example, the bill “Digital Commodities Exchange Act of 2022” clearly shows such movements. Under the bill, a registered DCE must monitor trading activity, prohibit abusive trading practices, establish minimum capital requirements, report certain trading information publicly, avoid conflicts of interest, establish governance standards, and adopt cybersecurity measures. The recent Basel Committee’s rules for banks is another example of such drives that aims to achieve regulatory compliance through imposing certain rules for banks and exchanges.

However, mixers and privacy coins will continue to remain an exception. OFAC’s (Office of Foreign Assets Control, an arm of the US Treasury) decision to include Tornado Cash in their sanction list, followed by the imprisonment of Tornado Cash’s developer Alexey Pertsev by Dutch authorities, took place because OFAC realized the protocol was directly being used for money laundering, allegedly by terrorist and hostile foreign organizations. This principle demonstrated by the regime will continue on.

Although not an argument, it is worth noting that censorship resistance has been seriously being discussed in the community since August. Active regulation such as the one introduced in Warren's bill will have to face fierce opposition from the industry–also linked with the recent worries that Ethereum is becoming less censorship-resistant with the recent OFAC measures.

Will KYC be applied more strictly on users and consumers (via frontend of the protocols towards US customers) of all of these DeFi platforms?

Yes. Regarding KYC on users themselves - requirements are already quite robust when it comes to US-based CEXs, and it’s more logical to assume these requirements will be extended to DEXs and DeFi protocols as a result of them being designated as digital commodity brokers or dealers - under future legislation. They will then be legally mandated to have KYC/AML checks on customers, and non-KYCd interaction with major DeFi protocols will become close to impossible. In the long run, every single platform will fall into one of two buckets:

Legal in the US after full KYC (see currently Coinbase). This would include DEXs, yield farming / lending platforms, P2E games, and more.

Illegal in the US, only accessible through VPN usage (see dydx currently). Website hosts and cloud providers could potentially even be banned from hosting these protocols within the US.

No, only around mixing protocols and CEXes. CEX KYC will be sufficient to monitor money-laundring/terrorist-financing schemes as well as monitoring systemic risks in the system. More institutional players will still need KYC through CEXes or institutional level registration under the government’s roster of some kind. However, retail investors will not need to conduct some other KYC process in each of the protocol’s frontends. Regulating the frontend of each DeFi protocol (highlighted in the recent debate between SBF and Eric as destructive to the whole industry) is not a possibility, and governments would not have much ground to do this.

The newest iterations of the DCCPA are broader and create more room for DeFi - lobbying activity is gaining momentum.

As shown through these two examples, the DCCPA’s broader language generally marks the DCCPA as more ambitious in terms of what regulatory authorities it may grant the CFTC, by virtue of the greater room it provides for the agency to interpret the legislation and create regulations enforceable against entities operating under its oversight.

Closing Remarks

The two main pillars of DeFi, LP tokens and staking derivatives, are very interesting in their nature and require much deeper understanding. In this debate piece, we have gone through which aspects of these assets are either closer to security or a commodity, as well as going through possible scenarios of regulation playing out in DeFi protocols with more focus on those that deal with these new digital primitives.

Recent crash of FTX and the other centralized exchanges thus pose questions on how KYC/AML will be implemented along with a more sound financial risk assessment of CEXes. Certain spillovers are also expected over certain DeFi protocols too. This is definitely a journey ahead of us, and we at FranklinDAO Research are very excited to build what’s to come.

Appendix A

Here we give brief introductions to the crypto bills that you need to keep track of.

1) DCEA (Digital Commodity Exchanges Act)

Reps. Ro Khanna (D-CA), Glenn Thompson (R-PA), Tom Emmer (R-MN) and Darren Soto (D-FL)

DCEA is a bill on how to regulate "digital commodities exchanges" aka centralized crypto exchanges (e.g. monitoring trading activities and measures to protect customers’ assets).

Two points to remember are:

- The bill gives CFTC exclusive jurisdiction over digital commodities and the right to decide whether certain assets fall under such category or not (=whether it can be considered a security).

- The DCEA would create an elective registration option for crypto exchanges to register with the CFTC. Platforms that register will be able to offer leveraged trading and digital commodities that were distributed to individuals before being available to the public.

2) DCCPA (Digital Commodities Consumer Protection Act)

Stabenow and Boozman

Once backed by SBF, still alive and worth noting. Key points are:

- Making it mandatory for crypto trading facilities to register with CFTC. (DCEA leaves it voluntary)

- Allowing the SEC to decide which tokens are securities (with exceptions)

3) RFIA (Responsible, Financial Innovation Act, aka Lummis-Gillibrand)

Another bill that has been in the spotlight. Although it gives CFTC exclusive oversight, there are many exclusions to it, such as NFTs, security-like tokens and stablecoins.

It would categorize DAOs as business entities for purposes of the tax code. This is significant in that it still leaves the door open for crypto assets to be classified as securities that “represent equity or debt interest to a business entity”

This piece by Ropes & Gray is a great summary of the bill:

4) Stablecoin bill by McHenry/Waters

Also worth noting in two aspects:

- It intends to give the Federal Reserve oversight over stablecoin issuers and

- It contains banning "endogenously collateralized" stablecoins. (what happens to FRAX and DAI now?)

This is quite interesting in that, in this framework, central stablecoin issuers will also work as an arm of the federal reserve’s bank, allowing for FED’s influence into the ecosystem. It’s not hard to imagine Circle taking part in the Money Market in the near future. These two lawmakers have been forming deep ties with Tether and Circle. Coindesk even picked them as the most influential figures in crypto of 2022

5) The Warren Bill

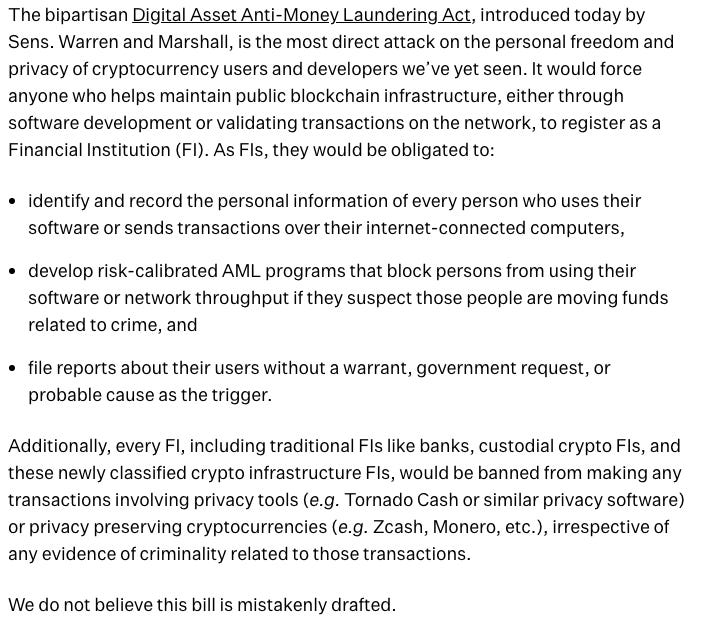

Warren’s crypto Bill (a.k.a. Digital Asset Anti Money Laundering Act of 2022) that was introduced as a response to the FTX collapse focuses on AML measures that aims to achieve greater compliance with the traditional finance regime.

The first line of opposition to this bill comes from the broad inclusion of ecosystem participants into the category of “money service businesses” who will be obliged to register as a Financial Institution and follow the AML compliance rules. Coin Center clearly opposes this in their recent piece.

This is also something not as seen explicitly in other past crypto bills, as node operators, contributors of the overall economy will be directly obliged under this law to implement measures themselves that will compromise censorship resistance of the crypto industry. This is not surprising, considering the fact that the previous version of the bill was called “Digital Asset Sanctions Compliance Enhancement Act,” and already contained measures to get rid of all the possible loopholes involving cryptocurrencies that circumvented the US government's AML regime. However, once passed, this will affect every single entity within the crypto space more towards the favor of the US government in censoring the ecosystem slowly.

Second line of opposition within the industry comes at requiring the Treasury Secretary to promulgate a rule prohibiting financial institutions from transacting with self-hosted wallets. This also comes from the fact that self-custody wallets are a useful method for money-laundering. However, after the FTX collapse, it seems quite ironic from a custody safety perspective to deter retail investors from using self-custody wallets.

Besides these two points, the bill also includes regulations around Digital asset Kiosk (ATMs) and Digital asset Mixers but has no clear claim on the jurisdiction between the CFTC and the SEC.

Appendix B

Here we provide a brief introduction to ongoing crypto court cases.

1) Ripple

Ever since the SEC sued Ripple’s Cofounder and Ripple’s CEO in 2020, the court case has been the representative case of crypto-security issue.

The fight here is in 1) whether the sale of XRP in the period 2013-2020 is considered to be an investment contract and 2) whether XRP satisfies the third and fourth clause in the Howey Test (“expected profit to be derived from the efforts of others”).

The case is expected to see come to a conclusion in the first half of 2023, and many are expecting Ripple’s wins. It’s interesting that Ripple emphasizes the quote from SEC’s expert that from mid-2018 onward, bitcoin and ether returns “can explain as much as almost 90% of XRP returns.” (and thus the investors are not expecting profit from investing in the token itself).

2) LBRY

On the other hand the recent LBRY court ruling was a shocking one indeed. The SEC has made their successful case of ruling a token as security, and it seems Ripple is trying its best to differentiate its tokens from LBRY.

A great thread on their different strategy (by @Belisarius2020):

3) Tornado Cash

This isn’t strictly a court case yet, but the significance of it mustn’t be ignored. OFAC’s designation of Tornado Cash in August has sparked the whole debate of blockchain censorship.

Some government-related parties have blacklisted all the addresses that have interacted with Tornado Cash. And there are an increasing number of validator who choose to follow rules imposed by the government. MEV and block-building are also deeply related here.

Moreover, in November, the Dutch court ruled that the Tornado Cash dev Alexey Pertsev stay in jail for another three months. This also gives us a glimpse of how DeFi products (that go against certain US regime) may end up.

4) OokiDAO

Now OokiDAO v CFTC. Although in its initial phase, the case has already bumped into a very special incident of CFTC serving the lawsuit via Chatbot and forum posts (it was originally allowed in October, but four amicus briefs were filed that are under process).

This case is following the settlement between CFTC and Ooki’s two founders under charges of “Offering Illegal, Off-Exchange Digital-Asset Trading, Registration Violations, and Failing to Comply with Bank Secrecy Act”.

This case is definitely important in that similar cases may also be applicable to other decentralized trading platforms such as GMX or GNS. It is also noting that this is unique in its case against the DAO itself.

A great thread on their latest hearing tweets by @nikhileshde

Great piece